A Biased View of Mortgage Company In Mississauga

The 2-Minute Rule for Mortgage Company In Mississauga

Table of ContentsOur Mortgage Company In Mississauga DiariesThe Ultimate Guide To Mortgage Company In MississaugaLittle Known Questions About Mortgage Company In Mississauga.Indicators on Mortgage Company In Mississauga You Need To KnowThings about Mortgage Company In MississaugaThe smart Trick of Mortgage Company In Mississauga That Nobody is Discussing

That head-to-head contrast among various choices is the very best method to make the right selection in one of the biggest purchases in your life - Mortgage company in Mississauga. The very best way is to ask good friends and loved ones for recommendations, however make certain they have actually utilized the broker as well as aren't just going down the name of a former university roomie or a distant colleague.Another referral resource: your property representative. Ask your representative for the names of a couple of brokers that they have dealt with and count on. Some property firms provide an internal home loan broker as component of their suite of services, yet you're not obliged to go with that firm or individual.

Check your state's expert licensing authority to ensure they have mortgage broker's licenses in good standing. Check out on-line testimonials as well as examine with the Better Company Bureau to examine whether the broker you're taking into consideration has a sound online reputation - Mortgage company in Mississauga.

Mortgage Company In Mississauga Fundamentals Explained

Can figure out which issues may create problems with one lending institution versus an additional. Why some buyers stay clear of home loan brokers Occasionally property buyers feel more comfy going straight to a big bank to secure their funding. Because situation, purchasers ought to a minimum of talk with a broker in order to understand all of their options pertaining to the kind of finance and also the readily available rate.

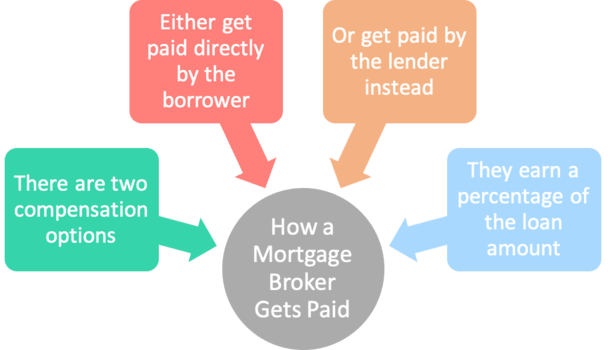

In many cases, customers prevent home loan brokers since they think they will certainly bear the expense of brokers' solutions themselves. The loan provider pays the compensation to the broker at closing, which is usually 12% of the quantity of the finance. There is a fairly tiny charge, often called a financing origination fee, paid by the consumer to the broker.

The Buzz on Mortgage Company In Mississauga

It is essential to be attentive when working with any kind of specialist, including a mortgage broker. Some brokers are driven solely to close as numerous finances as possible, hence jeopardizing service and/or values to seal each deal. Also, a mortgage broker will not have as much control over your loan as a big bank that finances the financing in-house.

When you buy a residence, specifically if you're doing it for the initial time, you do not want it to be a problem. So you believe to on your own: Just how can I make this as simple as feasible? I assumed the exact same thing when I bought a residence in 2016. It had not been my first time acquiring-- I would certainly owned a residence prior to with my ex-husband.

I obtained gotten in touch with a realty representative and also pretty quickly, located a residence I intended to make an offer on. As soon as my deal was accepted, the following action was obtaining a home mortgage. I could have gone right to my bank and also requested a home mortgage. Yet what I did instead was get to out to a home loan broker.

The Mortgage Company In Mississauga Diaries

What Home mortgage Brokers Do If you've never bought a home before, you may not understand what mortgage brokers are everything about. Right here's the offer: To do that, you need to offer the broker particular information, including: Consent to check your credit rating reports as well as credit report A duplicate of your most recent tax return pop over to this site Current pay stubs Your company's call information so they can confirm your work background That seems very easy enough? And also in exchange for providing the broker those details, they handle all the training published here of mortgage purchasing.

You don't need to invest hrs trying to find a funding since the broker is dealing with that. Home mortgage brokers' obligations Home loan brokers have expert knowledge and sources the average house buyer does not. They normally have a larger network of lenders they function with so they can actually drill down to what sorts of finances you're most likely to get and what rates of interest you're most likely to get.

How Mortgage Company In Mississauga can Save You Time, Stress, and Money.

Preferably, all you have to do is answer any type of follow-up inquiries the lending institution routes to the broker. The expense of making use of a home mortgage broker In return for doing all that,.

That way, you pay nothing out of pocket. Every one of that appeared terrific to me when I was all set to purchase once again. I was servicing growing my freelancing organization as well as elevating 2 youngsters and I just really did not have time to get stalled in the information of locating a mortgage.

An Unbiased View of Mortgage Company In Mississauga

About providing the broker some details about your home I desired to purchase, I was pre-approved for both a USDA and an FHA finance. Now: I felt like points were travelling along pretty well. Left in the dark I was really leaning towards the USDA funding, considering that those need absolutely no money down.

Which I did. By the time the broker obtained clued in as well as let me recognize, I 'd currently filled up out the complete home loan application for the funding, with the tough inquiries on my credit record to verify it. This has to do with a month right into working with the broker. While I was a little upset, I asked click here now for the next choice, which was an FHA financing.